Let’s address the elephant in the room, or rather, the 7% interest rate sitting on your kitchen table like an uninvited guest who won’t leave.

If you’ve been looking at buffalo homes for sale lately, you’ve probably had a moment where you stared at a mortgage calculator and thought, "Maybe I'll just live in a tent in Delaware Park." I get it. Compared to those "once-in-a-lifetime" 3% rates we saw a few years back, 7% feels like a personal insult.

But here’s the reality check: It is currently Wednesday, April 8, 2026, and the 7% mortgage rate is the new normal. The good news? Buffalo is still one of the most affordable housing markets in the country. While people in California are paying $1M for a literal toolshed at 7%, we still have incredible opportunities here, if you know how to play the game.

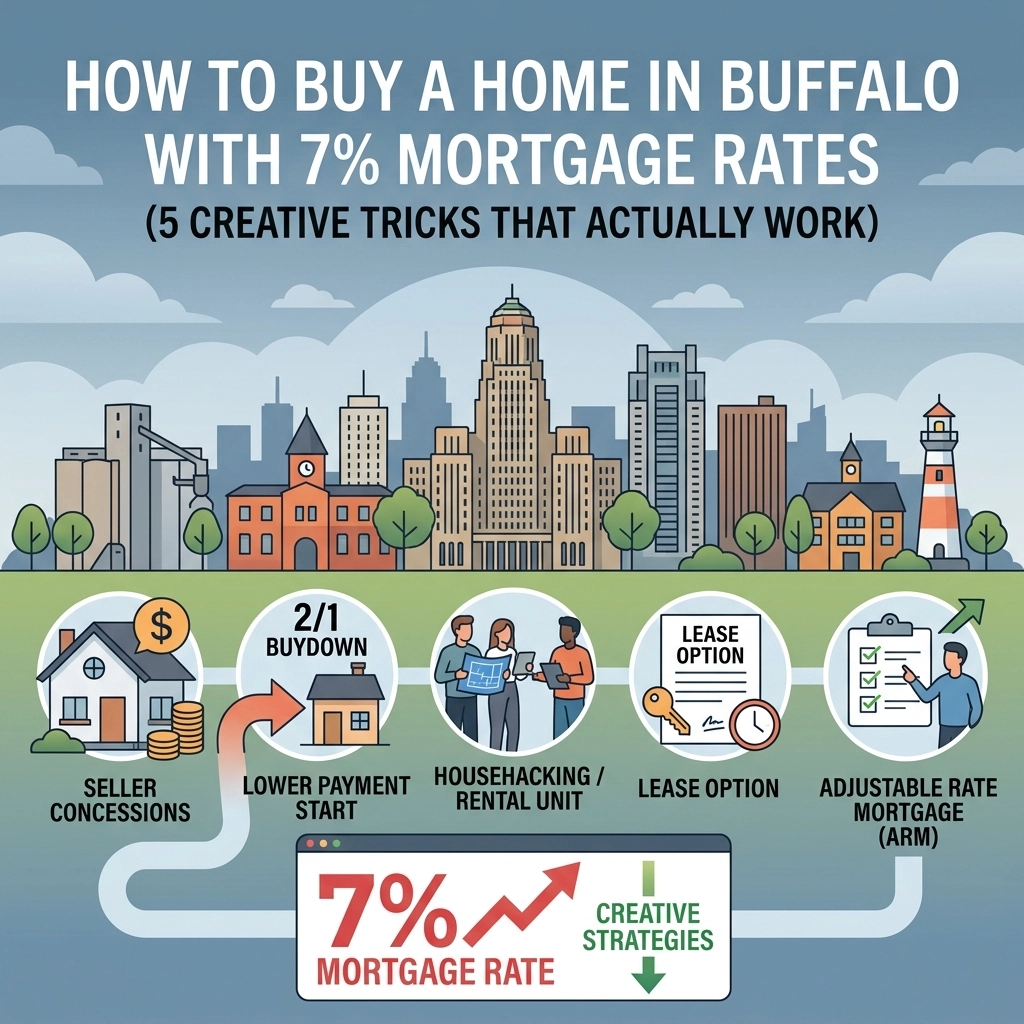

To buy a home in buffalo successfully in 2026, you can't use a 2021 playbook. You need a bit of strategy, a dash of creativity, and maybe a little bit of Buffalo grit. Here are five creative tricks that actually work to help you beat the "rate blues" and get those keys in your hand.

1. The 2-1 Rate Buy-Down (The "Rate Tease")

If you are a first time homebuyer buffalo ny, this is your absolute best friend. A 2-1 buy-down is a way to "cheat" the interest rate for the first two years of your loan.

Here’s how it works: You (or more ideally, the seller) pay an upfront fee to lower your interest rate by 2% in the first year and 1% in the second year. By year three, it goes back to the standard 7%.

Why does this matter?

- Year 1: You pay 5% interest.

- Year 2: You pay 6% interest.

- Year 3+: You pay 7% interest.

The goal here is simple: survival and refinancing. Most experts (and your favorite local realtor, me) anticipate that rates will eventually dip. By using a buy-down, you save hundreds of dollars a month now, giving you a "cushion" until you can refinance into a lower permanent rate later. It’s like a "Welcome to Homeownership" discount that you negotiate right into the deal.

2. Embrace the ARM (No, It’s Not a Dirty Word)

I know, I know. Mentioning an "Adjustable-Rate Mortgage" (ARM) to someone who remembers 2008 is like mentioning a blizzard to a Buffalonian: it triggers immediate PTSD. But hear me out: the ARMs of 2026 are not the same "exploding" loans of twenty years ago.

When you're trying to buy a home in buffalo today, a 5/1 or 7/1 ARM can offer a significantly lower starting interest rate than a traditional 30-year fixed mortgage.

The strategy is "Date the Rate, Marry the House." If you get a 7/1 ARM, your lower rate is locked for seven years. That is a massive window of time to wait for the market to shift or for your income to grow. If you don’t plan on living in the house for 30 years anyway (and most people don’t), why pay the 30-year fixed premium?

For a deeper dive into how this fits into the current local landscape, check out my 2026 Buffalo Real Estate Outlook.

3. The "Buffalo Double" Strategy (House Hacking)

If the 7% rate is eating your lunch, make someone else pay for the sandwich.

Buffalo is the land of the "Double": those beautiful two-unit properties that line the streets of Elmwood, North Buffalo, and South Buffalo. If you’re looking at buffalo homes for sale, don’t just look at single-family residences.

By purchasing a duplex, living in one unit, and renting out the other, you are "house hacking." In many cases, the rent from your tenant will cover 60-80% of your total mortgage payment. Suddenly, that 7% interest rate doesn't matter because your net out-of-pocket housing cost is lower than what you’d pay in rent for a tiny apartment in Allentown.

If you’re curious about which areas make the most sense for this, I’ve put together The Ultimate Guide to Buffalo Investment Properties, which highlights the neighborhoods where the math actually works.

4. Negotiate Seller Concessions Like a Pro

Back in 2021, if you asked a seller for a $5,000 credit toward your closing costs, they would laugh you out of the room (and probably sell the house to a cash buyer from New York City).

In 2026, the power dynamic has shifted. While it’s still a competitive market, sellers are more willing to talk. Instead of asking for a price reduction, ask for seller concessions.

Why? Because a $5,000 price drop only lowers your monthly payment by about $30. But $5,000 in seller concessions can be used to:

- Pay for that 2-1 buy-down we talked about earlier.

- Cover your closing costs so you keep more cash in your pocket.

- Pay "points" to permanently buy down your interest rate from 7% to 6.25%.

It’s all about how you structure the offer. I often tell my clients that the "sticker price" of the home is less important than the "effective cost" of the loan. For more tips on winning these negotiations, take a look at my guide on how to buy a home in Buffalo without losing a bidding war.

5. Pivot to Up-and-Coming Neighborhoods

If you’re dead-set on Orchard Park or East Aurora, you’re going to pay a premium. But if you’re a first time homebuyer buffalo ny on a budget, you have to look where the puck is going, not where it is.

Neighborhoods like the West Side, parts of South Buffalo, and even the "First Ward" are seeing massive investment. You can often find homes in these areas that are $100k cheaper than their suburban counterparts. When your loan amount is smaller, that 7% interest rate has a much smaller "bite."

For instance, the West Side has seen a total transformation. I’ve written specifically about the houses for sale on the West Side and how to navigate that specific market. Lowering your purchase price by $50,000 by changing your zip code is the most effective way to offset a higher interest rate.

Bonus Tip: Use Local Assistance Programs

Don't forget that Buffalo actually wants you to live here. There are programs like the City of Buffalo Down Payment and Closing Cost Assistance Program (DPCC) that provide up to $10,000 for qualifying buyers. If you can get $10k for free (pardonable after 5 years), it effectively cancels out the extra interest you’re paying in the short term.

Applying the 28% Rule

Before you fall in love with a porch, do the math. The "28% Rule" suggests your total housing payment shouldn't exceed 28% of your gross monthly income. At a 7% rate, your "buying power" is lower than it used to be. For a real-world breakdown of what your money gets you right now, check out my 2026 price guide comparing Orchard Park, East Aurora, and the West Side.

Final Thoughts: Should You Wait?

I get asked this every day: "Nick, should I wait until rates hit 5% again?"

Here’s my spicy take: No.

If rates drop to 5%, every single person who has been sitting on the sidelines for the last two years is going to flood the market. Demand will skyrocket, bidding wars will return to the "insanity level," and home prices will jump 10-15% in a single summer. You'll save on interest but pay way more for the house.

By buying now at 7%, you have less competition and more room to negotiate. You can use the tricks above to mitigate the rate, and then you can refinance when the market cools off. You can refinance a rate, but you can't "refinance" the price you paid for the house.

Ready to start the hunt? Whether you're looking for a classic Buffalo Double or a cozy starter home, I'm here to help you navigate the math and the market.

Reach out today at nicholascortorealtor.com and let's find your spot in the Queen City.